Introduction

The hours are the first thing anyone mentions about investment banking, and for good reason. The pay is high and the exit options are excellent, but the price is time, more of it than almost any other entry-level career demands. Before you sign up, or sit in an interview claiming you understand the job, it is worth knowing honestly what the lifestyle is really like: how many hours analysts actually work, why the work stretches so long, what the banks have done to rein it in, and whether the trade-off makes sense for you.

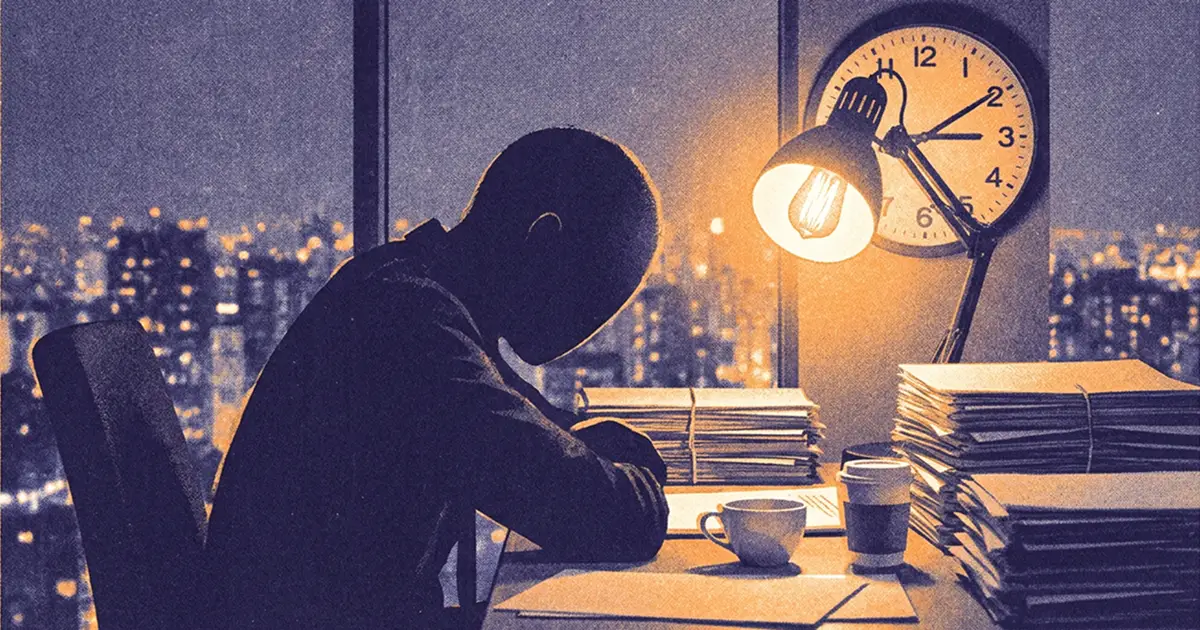

The short version is that a typical analyst works roughly 80 to 85 hours a week averaged over a year, with brutal stretches above 100 hours during live deals and genuinely quieter weeks in between. Since 2024, major banks have introduced 80-hour caps and protected weekends, but the underlying reality has barely shifted, because the work is driven by clients and transactions that do not keep office hours. What follows is the unvarnished version, the counterpart to the polished day in the life of an analyst: what the clock actually looks like, why it runs so long, and what to do about it.

How Many Hours, Really?

The "100-hour week" is the industry's signature myth, and like most myths it is part truth and part exaggeration.

The average and the range

Averaged across a full year, the median analyst at a major bank works something closer to 80 to 85 hours a week, not 100. But that average hides a wide range. Bulge bracket banks tend to run analysts at roughly 60 to 80 hours, elite boutiques like Lazard, Evercore, and Centerview push toward the higher end at 80 to 90 hours, and smaller regional boutiques can sit lower, around 50 to 70 hours in quieter stretches. The peaks are real: during a live deal, a hundred-plus-hour week absolutely happens, sometimes several in a row.

Why the hours are so unpredictable

The number that matters more than the average is the variance. Banking hours are spiky, not steady. A week can be calm until a client calls on Thursday wanting a revised pitch by Monday, and suddenly the weekend is gone. The unpredictability, more than the raw total, is what wears people down: it is hard to plan a dinner, a trip, or a relationship around a schedule that can be upended by a single email. The analyst seat sits at the bottom of the chain where all that last-minute work lands.

Why the Work Takes So Long

The hours are not long because banks are sadistic; they are long because of how deal work is structured and who drives it.

The nature of the work

Pitch books and models go through endless rounds of revisions, known as "turns." A senior banker marks up a draft, the analyst makes the changes, it goes back up, and more changes come down, often late at night and often repeatedly. Because the work is client-facing and high-stakes, it has to be perfect, and perfection through many iterations takes time. Much of the late-night work is this turning cycle.

- Pencils Down

A designated period when junior bankers are not expected to work, used by banks as part of their workload reforms. JPMorgan's policy, for example, protects the window from 6pm Friday to noon Saturday, though firms allow exceptions when a live deal demands it.

Client and deal timelines rule everything

Deals run on the client's clock, not the analyst's. When a transaction is live, with a signing or an announcement approaching, the team works whatever hours the timeline requires, including nights and weekends. Add global deals across time zones, where a European or Asian counterpart's morning is a New York analyst's late night, and the day stretches at both ends. The analyst, at the bottom of the hierarchy, absorbs the timing pressure that flows down from clients through MDs and VPs.

The ask

A VP or MD requests a model or deck, often late afternoon, for the next morning or a client meeting.

The build

The analyst builds it through the evening, frequently over dinner at the desk.

The turn

Comments come back at night; the analyst revises, sometimes through several rounds.

The wait

Juniors often cannot leave until senior bankers sign off, even during quiet gaps.

Repeat

On a live deal, the cycle restarts the next morning, for weeks at a stretch.

Know what you are signing up for: Practice over 1,000 interview questions and learn how the desk really works, download our iOS app to walk in prepared.

The Reforms: Caps, Protected Weekends, and Monitoring

The hours have been a live controversy for years, and a wave of reforms since 2024 has tried, with mixed success, to tame them.

What the banks introduced

After renewed scrutiny, major firms put formal limits in place. JPMorgan capped junior bankers' hours at 80 per week, layered on top of a Friday-evening-to-Saturday-noon protected window and a guarantee of one full weekend off each quarter, as Fortune reported. Bank of America also operates an 80-hour cap and built software requiring juniors to log their hours daily, naming the deals and the senior bankers involved. Goldman Sachs has run "Protected Saturday" policies along similar lines.

- Protected Weekend

A bank policy reserving certain weekend time, often Saturday, as off-limits for junior bankers, intended to guarantee a minimum of rest. Protected weekends are common across major banks but are routinely suspended when a live deal demands the work.

Why the reforms happened

The push gained urgency in 2024 after the death of Leo Lukenas III, a 35-year-old Bank of America associate and former Green Beret, who died of a blood clot while reportedly working more than 100 hours a week on a roughly $2 billion deal. The tragedy, alongside a Wall Street Journal investigation finding that juniors were sometimes told to under-report their hours, forced banks to act publicly.

Do the reforms actually work?

The honest answer is: only partly. Survey data from recruiters found that junior bankers reported working about as much in 2025 as they had years earlier, with first- and second-year analysts averaging roughly 78 hours a week despite the caps. The caps are widely seen as soft, suspended whenever a deal is live, which is much of the time. Tellingly, banks have moved toward enforcement by surveillance: JPMorgan began a program comparing juniors' self-reported hours against their actual computer activity, including video calls and keystrokes, according to CNBC. That a bank now monitors keystrokes to check whether the hours rules are being followed tells you how stubborn the underlying culture is.

How the Lifestyle Varies

"Investment banking hours" is not one experience. Where you sit changes it substantially.

By bank and group

Bank type matters: bulge brackets and elite boutiques generally run hardest, while regional and middle-market firms can be more humane. Group matters too. Active M&A and leveraged-finance teams in the middle of live deals tend to be the most demanding, while some capital markets desks run on more market-driven, slightly more predictable rhythms. Deal flow is the swing factor: a hot group in a busy year is brutal; the same group in a slow stretch can be almost calm.

By seniority

The hours do not simply vanish as you climb, but they change character. Analysts and associates carry the late-night production work, so they log the most hours and have the least control. VPs and above work long hours too, but more of it is client meetings, calls, and travel, with somewhat more control over their schedule. The trade is real: seniority brings more autonomy over your time even when the total hours stay high, which is part of what makes the grind survivable for those who stay.

Who controls your hours: staffing

Much of your week is decided by one person: the staffer. How you are staffed, on a hot live deal versus a slow pitch, on a demanding MD's team versus a reasonable one, swings your hours more than the bank's official policy does.

- Staffer

The person in a banking group, usually a senior associate or VP, who assigns analysts and associates to deals and projects. The staffer's decisions largely determine how busy any given junior banker is, which is why being staffed on the right, or wrong, deal team shapes your hours far more than headline policy.

The practical consequence is that two analysts in the same group, the same bank, and the same year can have very different lives depending on what they are staffed on. Building a good relationship with the staffer, and a reputation as reliable without being a doormat, is one of the few levers a junior banker actually has over their own schedule.

How Banking Hours Compare to Other Careers

It helps to see banking hours against the alternatives, because the comparison reframes the trade-off.

Versus consulting

Management consulting is demanding but in a different way. Consultants often work fewer raw hours, frequently in the 55 to 70 range, but trade them for heavy travel, typically away from home several days a week. The total intensity can be high, yet the work is usually more predictable than a live deal in banking, and the weekends are more often protected in practice.

Versus law and the buy side

Big-law associates face a comparable grind, driven by billable-hour targets and client deadlines that, like banking, can detonate a weekend without warning. The buy side is more varied: many private equity roles offer better balance than banking, but during a live deal or a fundraise the hours can rival anything in banking, and the work simply shifts from producing materials to making decisions under pressure. The point is that the elite, high-paying end of finance and professional services is demanding almost everywhere; banking is among the most intense, but it is not uniquely so.

Get the complete guide: Download our comprehensive 160-page PDF, access the IB Interview Guide covering the role, the recruiting process, and what the job actually involves.

Is It Worth It?

This is the question every candidate should answer honestly for themselves, because the trade-off is stark and personal.

On one side sits genuine reward: top-tier pay, an unmatched apprenticeship in finance, a powerful professional network, and some of the best exit opportunities of any career. Two or three years as an analyst can open doors to private equity, hedge funds, and corporate roles that would otherwise take far longer to reach. On the other side sits the cost: years of long, unpredictable hours, strained relationships, missed events, and real toll on health and sleep. Neither side is exaggerated, and the right answer depends entirely on what you want and what you can sustain.

It helps to be concrete about the cost rather than abstract. The hours come out of the same finite pot as sleep, exercise, relationships, and everything else, and for two or three years that pot is squeezed hard. People miss weddings, let friendships drift, and carry a chronic sleep deficit, and for some the strain on health and relationships simply is not worth any salary. Others find the intensity energizing, thrive on the steep learning curve, and barely register the sacrifice while they are young and unattached. Knowing which of those people you are, honestly, matters far more than any average hour count, because the same schedule that one analyst shrugs off can quietly break another.

How to Survive It and How to Judge It

If you do pursue banking, a few habits make the hours more bearable, and a few questions help you judge a firm before you join.

The survival basics are unglamorous but real: protect sleep where you can, build efficient working habits so you are not slow when work lands, manage up by communicating clearly about your capacity, and lean on your analyst class for support. The people who burn out fastest are often those who are disorganized under pressure or who have no outlet at all. Small things compound: keeping a clean model and template library so you are not rebuilding from scratch, batching revisions rather than touching a deck a dozen times, and being honest with a staffer about your bandwidth before you are underwater rather than after. None of it eliminates the hours, but it is the difference between long days you can sustain and a pace that breaks you.

Going in with an accurate picture is itself protective. The analysts who struggle most are often the ones who believed the hours were exaggerated; the ones who cope best expected them and planned their lives, and their two or three years, around the reality.

Key Takeaways

- Investment banking analysts work roughly 80 to 85 hours a week on average, with peaks above 100 during live deals and quieter weeks in between.

- The unpredictability matters more than the raw total: you rarely control your own time, because clients and deals set the schedule.

- The hours are long because of endless revision "turns," perfectionist client work, and global deal timelines that run nights and weekends.

- Since 2024, banks have added 80-hour caps, protected weekends, and even keystroke monitoring, prompted partly by a junior banker's death, but surveys show hours have barely fallen.

- The lifestyle varies by bank, group, deal flow, and seniority, with bulge brackets and elite boutiques on live M&A deals the most demanding.

- Whether it is worth it is personal: weigh the elite pay, skills, and exits against years of long hours and real strain, and treat the analyst years as a finite investment.

The hours are the defining feature of an investment banking career, and there is no point pretending otherwise. They are long, they are unpredictable, and the reforms have softened the edges more than the substance. But for many people the trade is a deliberate one: a hard, finite stretch in exchange for skills, money, and options that compound for the rest of a career. The worst mistake is to walk in surprised, expecting a normal job and then resenting the hours when they inevitably arrive. The analysts who fare best are rarely the ones who work the most; they are the ones who knew exactly what they were choosing. Know the reality, decide clearly whether it fits, and if it does, treat the hours as the price of an apprenticeship you took on with your eyes open.